The Goods and Services Tax Council (GST) at its 47th meeting convened a series of rate changes as part of the restructured tax rates with withdrawal of certain exemptions from what may be a precursor to a complete textile repairs and future adjustments.

What are the proposed changes?

|

Commodities/Items |

Hike from |

Hike to |

|

Household items such as LED lamps, printing/drawing ink, power driven pumps, Tetra Pak |

12% |

18% |

|

Solar water heaters, finished leather |

5%

|

12% |

|

Cut and polished diamonds |

0.25% |

1.5% |

|

Issuance of cheques |

0% |

18% |

|

Pre-packaged and pre-labelled food items |

0% |

5%

|

|

Orthopedic Appliances |

12% |

5% |

|

Ropeways services |

18% |

5% |

Other recommendations

|

Inverted Duty Structure: An inverted duty structure arises when the taxes on output or final product are lower than the taxes on inputs. |

Changes in the tax rate and rationalization of the tax rate will create both positive and negative impact on the Economy.

Positive impacts:

Negative impacts:

|

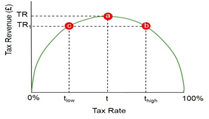

Laffer curve

|

Rising prices for daily commodities such as LED lights and packaged foods such as wheat flour, paneer, curd, lassi are expected to cause inflation in companies and are expected to add to inflation problems. On the other hand more revenue collection will provide a stable base for the more welfare schemes and scope for more expenditures. It is also important to consider the rationalization of the tax rate accordance with the Laffer curve to ensure better tax base with optimum tax rate.

Verifying, please be patient.